How to Classify Leases Correctly Under ASC 842

The ASC 842, or Accounting Standards Codification Topic 842, is the accounting standard for lease accounting in the

United States. It was issued by the Financial Accounting Standards Board (FASB) to improve transparency and

comparability of financial statements by recognizing lease assets and liabilities on the balance sheet. Under ASC 842

lease classification, leases are classified into two categories: finance leases and operating leases.

To

determine the ASC 842 lease classification, follow these steps:

- Identify the lease: First, determine whether a contract meets the definition of a lease under ASC 842. A contract is considered a lease if it conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

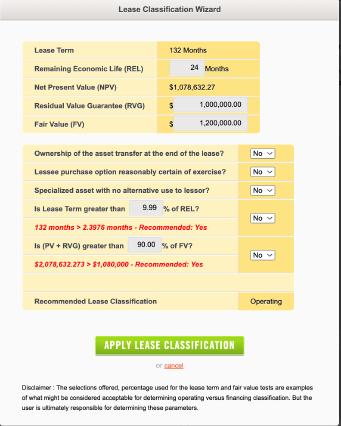

- Evaluate lease classification criteria: Next, assess whether the lease meets any of the five criteria for classification as a finance lease. If the lease meets one or more of these criteria, it is a finance lease; otherwise, it is an operating lease. The five criteria are:a. Ownership transfer: The lease transfers ownership of the underlying asset to the lessee by the end of the lease term.b. Purchase option: The lease grants the lessee a purchase option that the lessee is reasonably certain to exercise.c. Lease term: The lease term is for the major part of the remaining economic life of the underlying asset. However, this criterion is not used if the commencement date of the lease falls at or near the end of the economic life of the underlying asset.d. Present value of lease payments: The present value of the sum of the lease payments and any residual value guaranteed by the lessee that is not already reflected in the lease payments equals or exceeds substantially all of the fair value of the underlying asset.e. Specialized nature of the underlying asset: The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term.

- Classify the lease: Based on the evaluation of the criteria, classify the lease as either a finance lease or an operating lease.

- Accounting treatment: Once the lease classification is determined, apply the appropriate accounting treatment. Finance leases require recognition of a right-of-use asset and a lease liability on the lessee's balance sheet, while operating leases require recognition of a single lease expense on a straight-line basis over the lease term. Different rules apply to lessors, but they also classify leases as either sales-type, direct financing, or operating leases based on similar criteria.

Remember that the ASC 842 lease classification process may require significant judgment, particularly in

evaluating criteria like the lessee's certainty of exercising a purchase option or the lease term relative to the

remaining economic life of the asset. It is essential to consider all relevant facts and circumstances when classifying

leases under ASC 842.

iLeasePro simplifies the process to classify a lease!

Check out iLeasePro's ASC 842 Lease Classification Test Wizard

iLeasePro ASC 842 Lease Classification Wizard

Tour of iLeasePro

Schedule a Demo

Check Out Knowledge Base

Categories

- All Posts

- Audit (20)

- Close (5)

- Compliance (18)

- Controls (6)

- Disclosures (3)

- Financial reporting (4)

- Healthcare (4)

- Implementation (2)

- Lean accounting (17)

- Lease abstracting (3)

- Lease accounting (87)

- Lease analysis (14)

- Lease management (34)

- Press release (16)

- Product updates (9)

- Regulatory updates (31)